Why Powell was great, and my story of meeting him

Federal Reserve Chair Jerome Powell’s last press conference is today and his chair term ends in a couple of weeks. He will be sorely missed as chair, no matter if he stays on as Governor or not. I think he was great.

His greatness was a particular kind; amplified transparency, intellectual integrity, and authenticity; sustained for almost a decade through everything that should have broken it. Transparency isn’t just a virtue at the Fed, it’s what gives their words enough credibility to amplify rate decisions and change policy quicker — because they do what they say they will do. Former Fed Chair Ben Bernanke spent his chairmanship inventing that (and QE for the US); pushing the Fed toward transparency, the post-meeting statement, the press conference, the summary of economic projections. Bernanke built the structure. Powell took those ideas, refined further by Yellen, and elevated them.

Bernanke himself praised Powell for this. In May 2023, the two of them sat on stage together, predecessor and current Chair, and Bernanke walked through the communications tools he had introduced during his own tenure. He said the post-meeting press conference was something Powell “has taken to an art form.” A Nobel laureate predecessor, on stage, handing his successor the credit for elevating the thing he himself built. Peers don’t say that lightly.

The press conferences were the demonstration of this. Eight a year, almost a decade, through a pandemic, an inflation surge that nobody saw coming clearly, a banking crisis, tariffs, and a rate cycle that should have broken a lesser communicator. Powell was perfectly transparent the whole time. He told the public what the Fed was doing, what the data showed, what would change his view, and what would not. Even when he was wrong, you knew what the wrong thing depended on. When the data turned, the structure let him turn with it without contradiction. He said true things in a careful structure, and the structure itself was the art.

The phrase that stays with me is “statistical regularity.” In late July 2024, unemployment was ticking up and the Sahm Rule was about to trigger. The press wanted Powell to say recession was imminent. He was asked directly. His answer, in the July 31st, 2024 FOMC press conference, was that the Sahm Rule was “a statistical regularity,” not “an economic rule where it’s telling you something must happen.” That is a real distinction, compressed into two words, delivered on camera, in real time, while every reporter in the room was trying to get him to commit to a worse outlook. Empirical regularities from the past are not laws of nature. He said it cleanly and he was right.

Powell gets criticized for being late on inflation in 2022. Larry Summers warned in February 2021 that the fiscal package was too big and that inflation was coming, and he was right. But the critique misses the problem at the time. The size of the pandemic’s shock to the economy was genuinely unknown in 2020 and 2021, and the risk was asymmetric. Under-reacting to a serious pandemic is far worse than overstimulating, and nobody really knew what would happen. The Denver convention center down the street from me was converted into a field hospital that was never used. Nearly everyone made the same call in the same direction: Congress, the White House, the CDC, Governors, Mayors, and most economists who weren’t named Larry Summers. Powell accommodated for that asymmetric risk, and given what was knowable, he did the best he could. If the situation were played back again knowing what we know now, few would repeat the actions they took then.

As the economic shock turned out to be up rather than down, the picture changed. The Fed hiked 525 basis points in sixteen months, often 75bps at a time, the fastest tightening cycle in forty years, which was apt. Powell stood at the podium meeting after meeting saying clearly what the Fed was doing and why. He absorbed the political cost, he answered the unanswerable questions with poise. He responded to what he knew, changed when the data changed, and conveyed the shift as it happened.

Then President Trump came for him for easier monetary policy, a trope of history. LBJ pressured William McChesney Martin in 1965. Nixon pressured Arthur Burns in 1971-72 and got the rate cuts that helped fuel the inflation of the 1970s. Reagan’s Treasury Secretary James Baker tried to order Volcker not to raise rates. George H.W. Bush blamed Greenspan for his 1992 election loss. Trump went after Powell in his first term too.

But what came in Trump’s second term was different in scale: years of personal attack, public name-calling, threats of firing, and finally a Justice Department criminal probe over renovation of the Fed building, dressed up as concern about cost overruns and accusing him of lying to Congress. Powell handled this with grace and without taking his eye off his day job. Just this January, he went on camera and said the probe was about whether the Fed could continue to set rates “based on evidence and economic conditions, or whether instead monetary policy will be directed by political pressure or intimidation.” That was not the language of a man trying to keep his head down. That was a sitting Chair calling out the President of the United States, on camera, in his own voice, with the full dignity of the institution behind him.

The institution agreed. Every living former Fed Chair, Bernanke, Greenspan, Yellen, signed a joint statement with former Treasury Secretaries Geithner and Paulson and former Council of Economic Advisers chairs from administrations of both parties, defending Powell. They wrote that the kind of pressure Trump was applying was “how monetary policy is made in emerging markets with weak institutions” and that it had “no place in the United States.” The next day, the rest of the world’s central banks added their own statement of solidarity. Christine Lagarde of the ECB, Andrew Bailey of the Bank of England, Tiff Macklem of the Bank of Canada, Martin Schlegel of the Swiss National Bank, plus the central bank governors of Sweden, Denmark, Australia, South Korea, and Brazil, along with leadership of the Bank for International Settlements, said they stood “in full solidarity with the Federal Reserve System and its Chair Jerome H. Powell.” Then just last week, a federal judge, James Boasberg, looked at the subpoenas and ruled them pretextual, finding “essentially zero evidence” of any crime and a “mountain of evidence” that the dominant purpose was to harass Powell into yielding or resigning. The probe was dropped. Powell held the line.

Volcker broke inflation. Greenspan was the maestro. Bernanke had the crisis playbook and the intellectual depth. Yellen refined the framework with academic precision. But Powell may be the first Fed Chair who let the public see the Fed thinking in real time without any guard, in the right words, every meeting, for years, without ceding an inch of the Fed’s independence, while a sitting President tried to break him in public. Powell was the best of any chair at avoiding what I call “narrative fill”, which is the tendency to reach for lower-quality arguments when the high quality ones aren’t supportive. Powell respected that those listening to him knew as much as he did — a much harder position to sustain and one that future chairs hopefully build on.

That is the Powell I read about and watched. The one I met was the same man, ten years earlier, waiting for an elevator.

In October 2014, the Treasury market had a flash rally. The 10-year moved something like 37 basis points intraday for no good reason, and the people who run the plumbing of the U.S. Treasury market and large investors at the central bank level noticed. A year later, the New York Fed, the Treasury Department, the SEC, the CFTC, and the Board of Governors put together a two-day conference to figure out what had happened and what the market had become. October 20 and 21, 2015. It was the first one. They have run it every year since.

The conference was invite-only and oriented to larger institutional buyers. Kessler was smaller and Denver-based but Treasuries only, so I wrote to ask if I could come. They said yes. I got on a plane to Manhattan.

The New York Fed building is its own experience. Limestone and ironwork on Liberty Street, guards with machine guns at the doors, more gold in the basement than Fort Knox. You walk in and you can feel the weight of the place. This is the Fed branch where the rubber meets the road — where the Fed target rate is guarded in the market. I went through security and rode the elevator up to the twelfth-floor auditorium with a buzz I get when I am somewhere that matters.

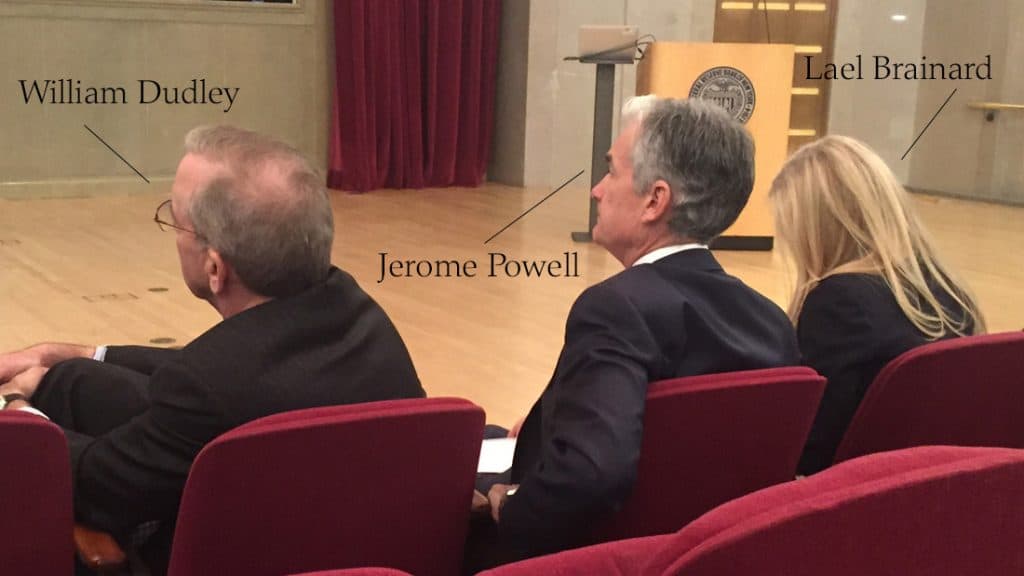

The morning opened with Bill Dudley, who was running the New York Fed, and then Powell beamed in on a live video call from Washington. He was scheduled to be there in person but something had come up, and he would join us in the afternoon. The video call itself felt like high-end IT at the time. A few hours later he was in the room. The whole conference, I realized, was to reassure the buyers that matter.

I sat two rows behind Dudley, Powell, and Lael Brainard for most of it. They were stars to me, and I was watching them work.

On the second afternoon, Powell moderated the panel on repo markets. Beth Hammack from Goldman was a panelist, ten years before she became Cleveland Fed President. Lorie Logan from the NY Fed had moderated a panel the day before, seven years before she became Dallas Fed President. The room was the next generation of Fed leadership being seasoned alongside Powell himself. And then it was over.

The auditorium empties into a big hall that leads into the elevator bank. Everyone was funneling toward the elevators but only a few could go at a time, so we’d all backed up into the hall and were waiting. Somebody nearby said, “this is normal, just be patient.” It was going to be a while. I look over and the thin Jerome Powell is standing right next to me.

I said, “Wow, a real-life Governor. I’m star struck.”

He turned to the guy next to him, his aide, and joked, “we don’t get that a lot.” He was being demure. Then he turned back to me and asked where I was from and what I was doing. I told him about Kessler, about Denver, about the work I do. He was interested. We stood there for a few minutes, the three of us, laughed and had a moment. He was warm and easy and entirely a person.

I learned later that the unsaid rule of those rooms is that everyone acts like they do not notice it is a big deal to be there. The Governors are colleagues, the gold in the basement is a footnote, the conference is just a thing on the calendar. I also realize that for some, this is their rhythm of life, but it wasn’t for me. I said the true thing, which was that I was star struck, and saying it allowed us to have a fun moment as people.

The man at the podium for all these years and the man in the elevator line were the same man.