Insights

U.S. Interest Rates Commentary and Research from Eric Hickman

This material is provided for informational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell futures/securities. The material is not intended to be used as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s account should or would be handled, as appropriate investment strategies depend upon the client’s investment objectives.

{kind=link}

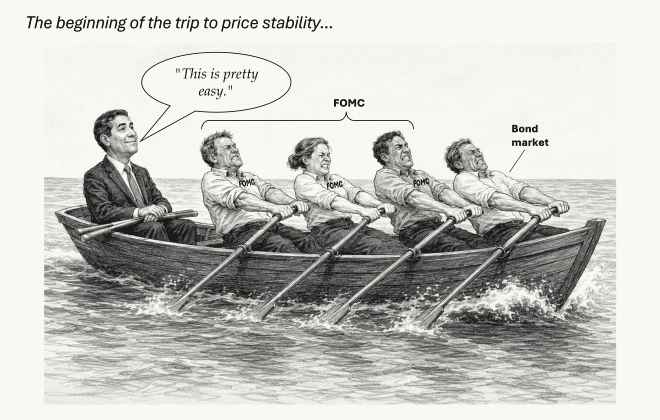

“The beginning of the story” – FOMC meeting review

Warsh was hawkish, the bond market didn’t quite get it, but the Fed is moving towards price stability with the reaction anyway. I realized today that I haven’t written a longer public piece since the last FOMC meeting. The reason is that rates have done…

{kind=link}

FOMC review: a hawkish committee with a new chair in tow

Warsh in the role Back in January, former Atlanta Fed President, Raphael Bostic, made a great prediction about Kevin Warsh; to not take his job-auditioning comments too seriously. In an interview with CNBC on 1/30/2026, Bostic said, I do think though, that we have to…

{kind=link}

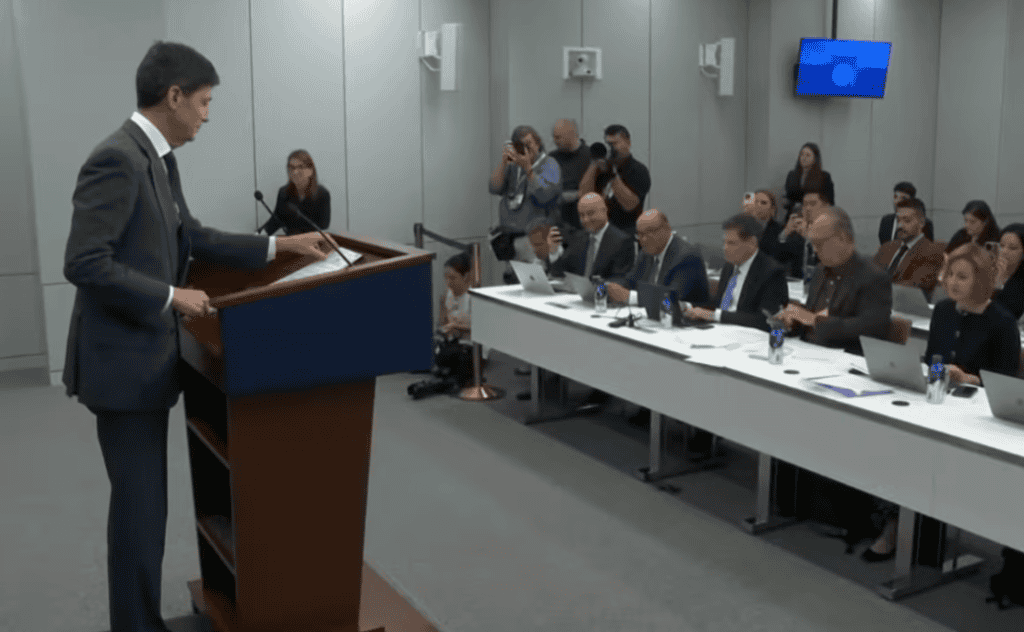

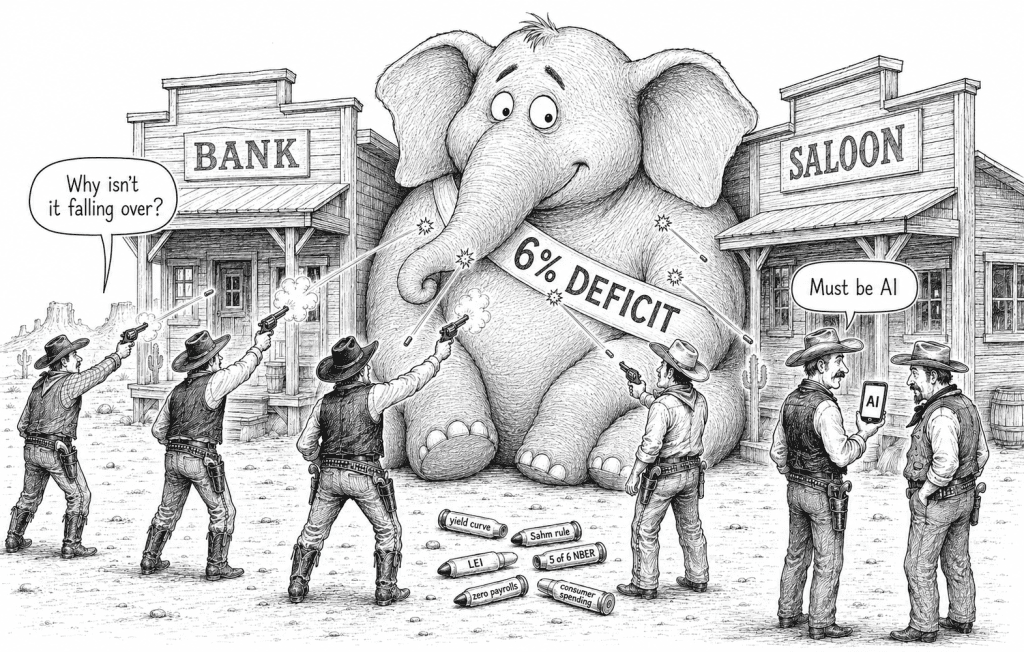

AI isn’t carrying this cycle, the deficit is

We all feel it We’ve all watched unusual buoyancy in equities for years. The stock market keeps absorbing more bullets than it should withstand. Bank failures, tariff shocks, private credit, Iran, recession scares, the data going soft, the Fed pivoting, unpivoting. Stocks higher through all…

{kind=link}

Why Powell was great, and my story of meeting him

Federal Reserve Chair Jerome Powell’s last press conference is today and his chair term ends in a couple of weeks. He will be sorely missed as chair, no matter if he stays on as Governor or not. I think he was great. His greatness was…

{kind=link}

Watch the PE cycle

The broad force behind stock market returns that nobody talks about. The S&P 500 made a new high last week. The economic expansion has stretched to a full six years this month despite five recession scares in the last three. The always-bullish consensus feels vindicated….

{kind=link}

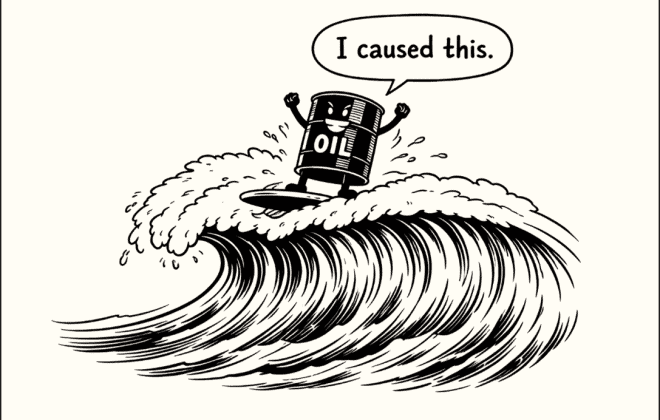

Oil isn’t the variable to worry about with the economy

A prominent new book on recessions and a recent piece by Niall Ferguson argue that energy shocks are among the most reliable causes of recessions, a thesis that has found a receptive audience given the Iran war and the sharp rise in oil prices that…

{kind=link}

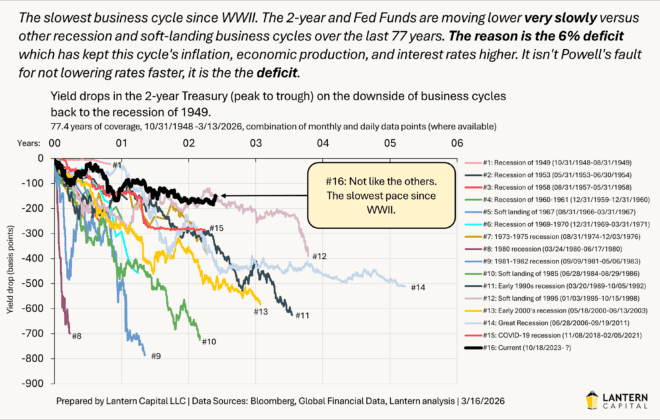

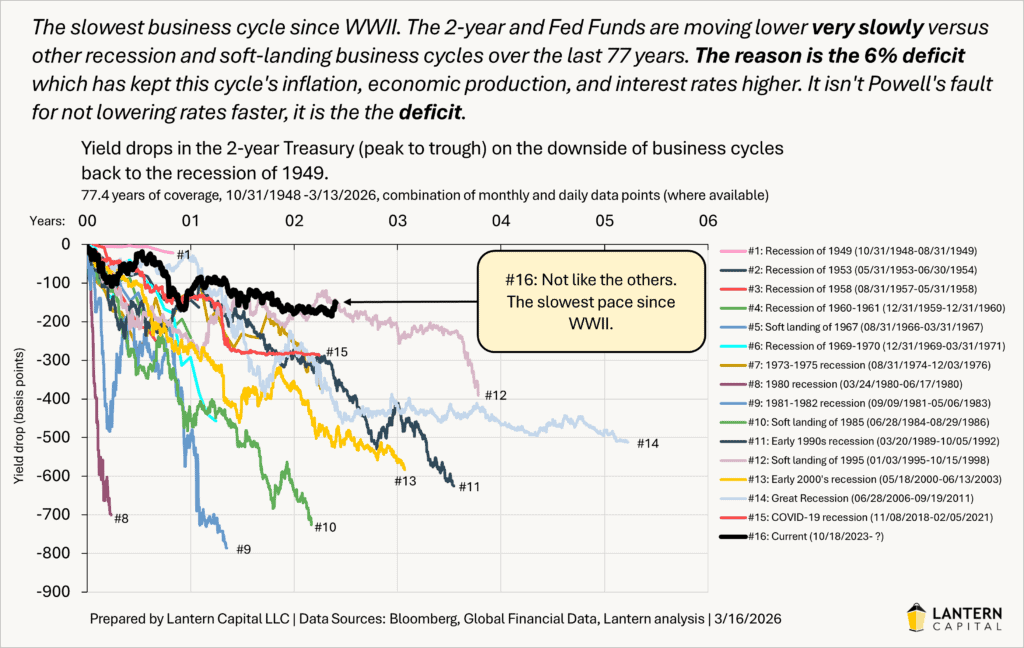

The Slowest Business Cycle on Record

Also on Advisor Perspectives Summary: Comparing business-cycle-related primary trends of the falling 2-year Treasury yield shows that this is the slowest business cycle since WWII (WWII is a rough place where Treasury yield data and an independent Fed began). In general, business cycles were sharper and…

{kind=link}

3-yr rate call performance

This writing presents the value of my interest rate calls back to November of 2022 (3.2 years ago) where I first advocated owning US Treasury duration in anticipation of rates falling in the ongoing, but slowly evolving, downside of this business cycle (note: I define…

{kind=link}

Skeptical of Truflation’s disinflation

Truflation is a newer private real-time statistic of inflation that comes out each day (similar to the LDEI) with more granularity to see trends changing faster, be more timely, and fill-in when official data is absent (like last year’s government shutdown). Since its inception in…

{kind=link}

The Fed moves to neutral with an upbeat forecast

In my piece before the Fed meeting, I expected the Fed/Powell to acknowledge economic improvement with short-term yields rising. I got half of that right. The Fed acknowledged economic improvement in the statement and press conference, but not to a degree that moved interest rates….