Oil isn’t the variable to worry about with the economy

A prominent new book on recessions and a recent piece by Niall Ferguson argue that energy shocks are among the most reliable causes of recessions, a thesis that has found a receptive audience given the Iran war and the sharp rise in oil prices that has accompanied it. The argument has intuitive appeal and historical support. But a careful reading of the three most cited cases, 1973-74, 1979-80, and 1990, raises serious questions about whether oil price spikes cause recessions or whether they simply arrive when conditions are right.

The distinction matters to whether one is imminent or not.

The business cycle as the ‘always’ force

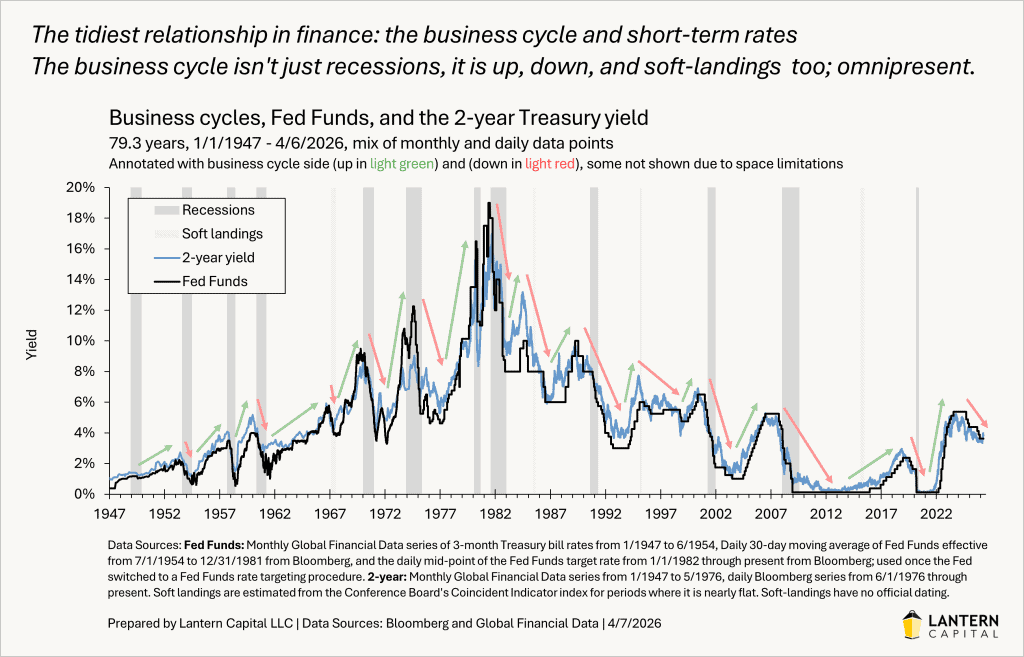

Before examining the historical cases, the business cycle needs to be appreciated for more than just recessions, a precept that often confines academic work. Studying the 2-year Treasury yield shows the full business cycle: up, down, and sideways in a more apt framework. The chart below shows 79 years of the relationship between short-term interest rates and the business cycle. It is what I call “the tidiest relationship in finance,” and shows something important: a continuous wave of roughly equal length for uptrends and downtrends, repeating regularly. The 2-year Treasury yield and the Federal Funds rate trace a clear and repeating wave pattern, up, down, recession or soft-landing, repeat, across nearly eight decades of wars, oil shocks, financial crises, and pandemics. The primary trend of the 2-year Treasury is a better segmenter of the business cycle than GDP, because it captures soft landings, segments the cycle more evenly, and reflects the economic deterioration that typically precedes and follows formally declared recessions. Recessions or soft landings have happened on average every five years since WWII. That regularity is more than a coincidence. It is the cycle running on its own clock, independent of whatever idiosyncratic event happens to be dominating the headlines at the time. It is hard to argue that this whole cycle only exists because of idiosyncratic events.

While it is seductive to think that avoiding economic shocks avoids recessions, the business cycle is always there. The downside can be mitigated by monetary policy, slowed by fiscal policy, or even effectively bought out by fiscal policy as in 2020, but never permanently suspended. It runs in the background whether we acknowledge it or not. And when a recession arrives, we want to assign it a cause: the oil shock, the dot-com bubble, the subprime mortgage crisis, the pandemic. We convince ourselves that if we can avoid the event, we can avoid the recession. That isn’t supported by the data.

1973-74: the mis-dated recession

The Arab oil embargo began moving oil prices in October 1973, one month before the NBER dated the business cycle peak in November 1973. On the surface this looks like classic causation. But the recession didn’t really begin until almost a year later.

Three of the four monthly indicators the NBER used (it uses six now) to date recessions held up until late summer and fall of 1974. One of the four, non-farm payrolls, didn’t peak until July 1974 and didn’t start falling at pace until November 1974, a full year after the embargo began. Real consumer spending fell from September 1973 to February 1974 but then recovered 81% of that decline into August 1974 before falling again. The unemployment rate didn’t start rising at pace until September 1974.

Short-term yields tell the same story. The Fed raised rates for the last time on July 15, 1974, and the 2-year yield peaked for the cycle in August. The tightening cycle didn’t end until the true economic weakness arrived, which makes sense. Because of the NBER recession dating, many point to this episode as the quintessential evidence of stagflation, where the Fed had to raise rates during a recession. With this detail taken into account, they didn’t raise in a recession at all.

Contemporaneous newspaper accounts confirm the confusion. A New York Times editorial from July 22, 1974, titled “Recession or Spasm?“, captures the uncertainty precisely. The Commerce Secretary was still arguing there was no recession at all, calling it an “energy-related spasm.” The editorial, while disagreeing, acknowledged that economic weakness stemmed from “more than the rise in oil prices.”

The administration was closer to right than history has given it credit for. A recession didn’t really arrive until late 1974. Considering the timing, the 1973-75 recession didn’t really begin until 4.7 years after the prior recession, nearly exactly the historical average of five years between cycles. The business cycle was due. The Arab embargo arrived into a cycle that was already aging, not into a healthy mid-expansion economy.

1979-80: part of the economy turned over first, then the Volcker shock

The 1979-80 case looks the strongest in the conventional narrative. Oil prices rose sharply from April 1979 to April 1980, and the U.S. entered recession in January 1980. The causal chain looks clean.

But almost a year before that recession began, and just as oil prices were starting to rise, a New York Times editorial was already expecting a recession. Two of the four NBER recession indicators had peaked in March 1979, before oil prices began to rise. In an editorial titled “Surrendering to Recession,” published April 13, 1979, the Times wrote:

When the nation’s seventh postwar recession begins sometime in the coming months, some will call it an accident of the Administration’s over-restrictive economic policy. But it was the unwillingness of both the Administration and Congress to take inflation seriously that has made recession inevitable.

Paul Volcker was then appointed Federal Reserve Chairman in August 1979 and immediately signaled the most aggressive monetary tightening in postwar history. The mid-point of the federal funds rate target rose from 11% when Volcker took over to 16.5% by March 17, 1980, just seven months later. That tightening was certainly part of the cause of the 1980 recession. The Iranian revolution contributed to an inflationary environment that gave Volcker both the justification and the political cover for tightening as aggressively as he did. Oil was in the chain of events, but monetary policy tightening at least partially caused the recession.

Once again, the 1980 recession arrived 5.3 years after the prior recession really began. The cycle was due.

1990: the recession that preceded the oil spike

The 1990 recession is widely misunderstood. It is typically presented as a direct consequence of the Gulf War oil spike. But a careful reading of contemporaneous accounts shows that recessionary conditions were already developing two months before oil prices started rising in early July 1990.

The Federal Reserve had already lowered rates 150 basis points from a recession scare the year before, so the economic community was already on recession watch. President George H.W. Bush expressed concern about recession on May 9, 1990, after two weak jobs reports, admittedly with the political incentive of wanting the Fed to cut rates. More tellingly, Federal Reserve Governor Martha Seger, without any such incentive and bucking the rest of her colleagues, warned on June 10, 1990 of dangers posed by economic weakness. As the New York Times reported the next day, she told a Bank for International Settlements meeting in Basel, Switzerland that “there have been isolated weak spots before in the seven and a half years of American economic expansion, but now several important sectors are showing a slowdown at the same time.”

That was nearly two months before the first Iraqi tank crossed into Kuwait and three weeks before oil prices began to move. Labor, retail sales, and housing indicators were all weakening before the business cycle peak was dated in July 1990. The oil spike landed on an economy already rolling over. The yield decline that followed wasn’t the bond market responding to a resolved conflict. It was pricing a recession that was already in motion.

The 1990 recession began 5.4 years after the prior soft-landing. Again, it was due.

The pattern across three cases

Three different circumstances, three different ways the simple oil-causes-recession story breaks down on close examination.

In 1974, the recession arrived on the cycle’s own schedule, nearly a year after the oil shock hit, suggesting the embargo was a contributing factor rather than a cause. In 1980, the oil shock came after two monthly NBER recession indicators had already peaked and fed into a Volcker tightening that induced the recession, one step further removed from direct causation than the conventional narrative suggests. In 1990, the recession was already in motion before the first barrel was disrupted, with a historically important Fed Governor warning of simultaneous sectoral weakness months before the invasion.

In each case, what the conventional narrative assigns to oil is more accurately assigned to the business cycle running on its own clock. The oil shock gets the billing. The cycle is the real actor.

The clearest impact of an exogenous shock like an oil spike is compositional rather than aggregate: energy prices rise, discretionary spending falls by a roughly commensurate amount, and the nominal economy is largely left intact. Inflation goes up and real growth comes down, but nominal GDP — the measure the business cycle actually runs on — stays roughly unaffected. That is a very different claim than oil causing a recession.

The current instance

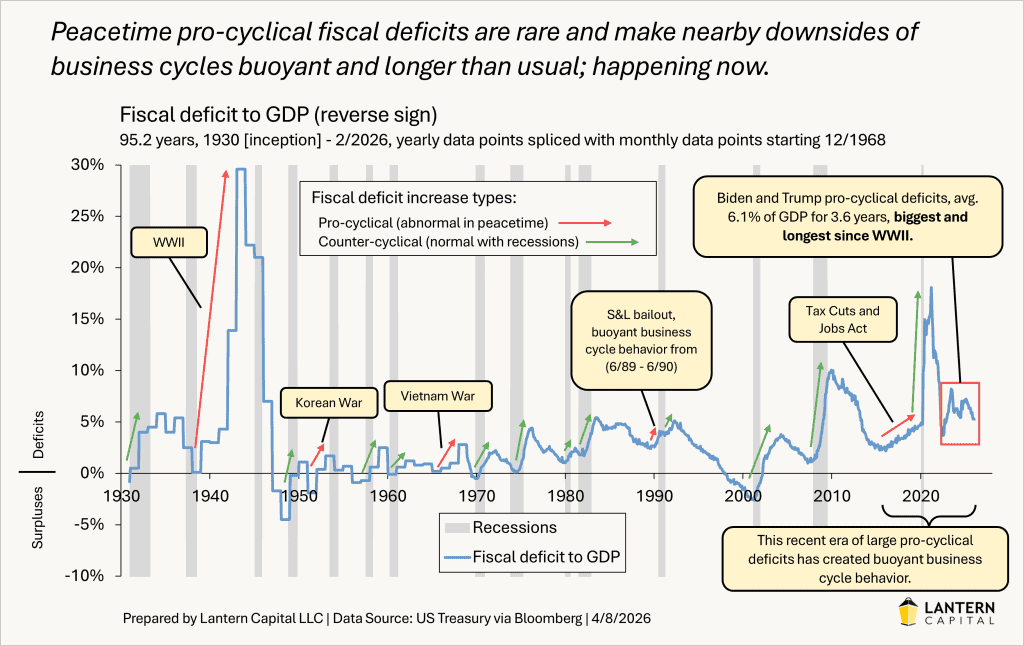

Which brings us to now. Given everything above, you might expect for me to be calling for a recession and lower rates imminently. The business cycle is on its downside, with the 2-year having peaked in October 2023. We just passed the six-year anniversary of the last recession. Everything in the historical record reviewed above would seem to point toward imminent recession. But as I have previously argued, and this will make Sir John Templeton turn over in his grave, this time is different. Not just a little different. Really different. Over the last three years the economy has defied five sure-thing recession indicators and is producing the slowest downside of the business cycle on record. It makes perfect sense when you consider that the fiscal deficit has averaged 6.1% of GDP over the last three and a half years. The US hadn’t had a pro-cyclical peacetime deficit over 3.5% of GDP until 2018. This one is nearly twice as high and has been sustained for more than three years with no end in sight. The deficit keeps the economy more buoyant than underlying conditions would otherwise support. Its vector is pointed up and its length is long. It doesn’t cancel the cycle, but makes it move like molasses.

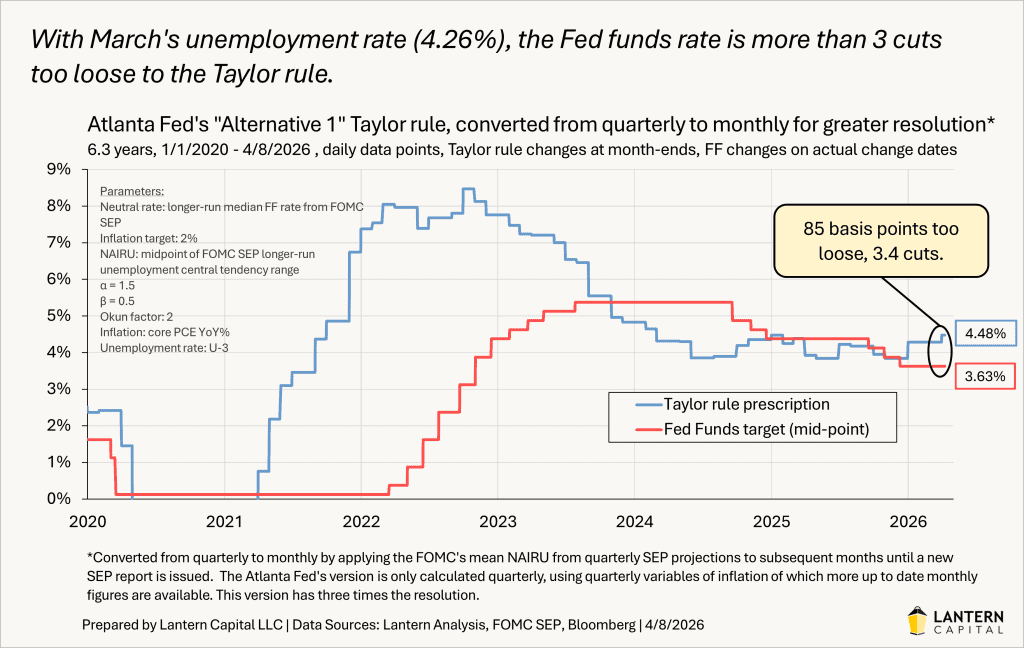

Since the cyclical peak in yields in October 2023, there has been a cycle within the cycle: whenever rates fall roughly 100 basis points in a recession scare, as they did late last year when the Fed cut three times, those lower rates have sparked a new recovery. As things have improved and inflation has gotten hotter since last fall, the Taylor rule suggests the Fed is about three cuts too loose relative to current economic conditions. That cycle within the cycle is still strengthening.

My view is that a recession is more likely toward the end of 2026 than now. Not because the oil spike won’t cause damage, it will cause some. But because the fiscal support keeping this expansion alive is still solid. Only one of the six NBER monthly recession indicators is below recent peaks, the household survey employment measure. Despite the appearance of a moment when recessions typically occur, the deficit supplants that timing.

A key assumption underlying this forecast was that the current oil price spike would prove temporary. The Strait of Hormuz carries roughly 20% of global oil supply. The economic consequences of keeping it closed fall on virtually everyone — the Gulf states, Asia, Europe, and ultimately Iran itself. The incentive structure made some resolution virtually inevitable, and yesterday evening, it arrived. With less than two hours to spare before a threatened US military strike, a ceasefire was announced, brokered through Pakistan. Iran agreed to the complete and immediate opening of the Strait of Hormuz. The market response this morning was immediate and telling: WTI crude fell 15% to $96, one-year inflation expectations dropped 39 basis points, and the S&P 500 rose more than 2%. Yields, however, fell only minimally — between 1 and 4 basis points across the curve.

That last detail is the most important one. If the oil spike had been the primary economic force, its removal should have produced a significant rally in bonds. It didn’t. The reason is that the underlying cycle — strong economic data, high service-sector inflation, a Fed that remains too loose by Taylor rule standards — was always the dominant force. The Wall Street Journal’s Nick Timiraos noted this morning that the ceasefire paradoxically narrows the path to near-term Fed rate cuts, because it removes the demand destruction risk without removing inflation pressure. That is precisely the “cycle-first” argument. The war arrived into a backdrop that was already pointing toward higher rates. The beginning of its resolution confirms that the backdrop remains intact.

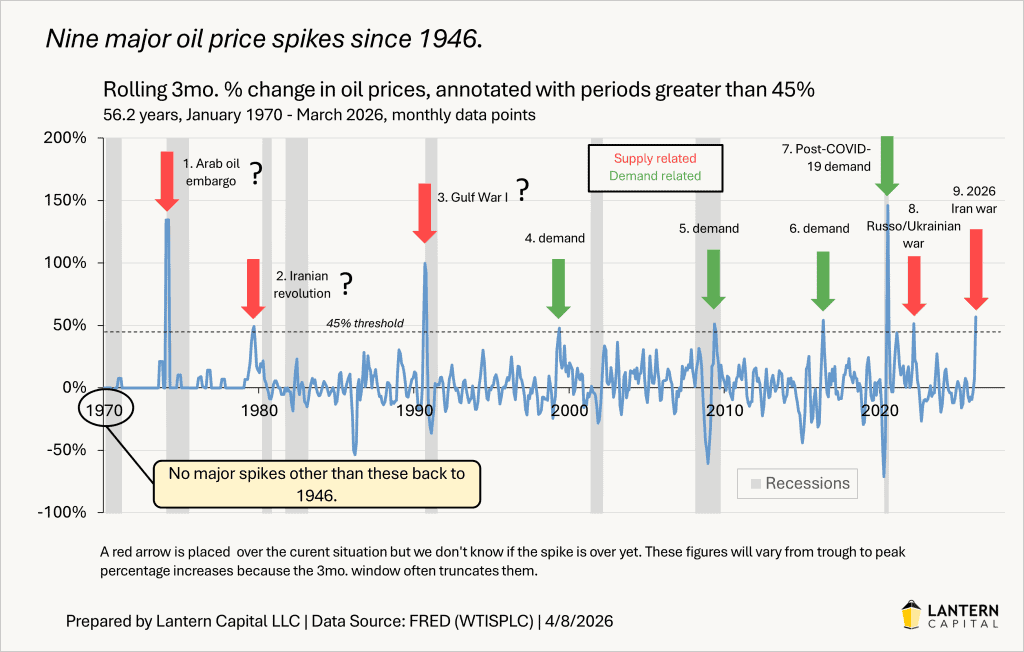

Besides which, oil price spikes happen regularly without recessions nearby. Of the nine times since 1946 that oil prices rose more than 45% over three months (like now), four were caused by strong demand and one supply shock, the Russia-Ukraine war, had no recession for years on either side of it.

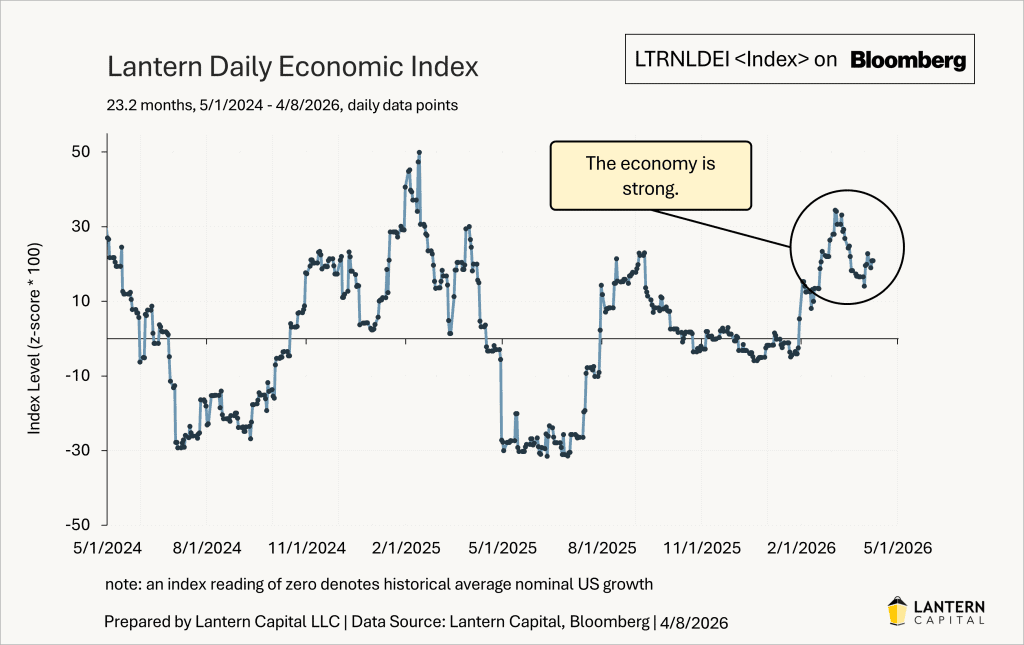

The real variable to watch is the Lantern Daily Economic Index (LDEI), which tracks daily economic activity across 45 indicators of the nominal economy. A natural question is what the LDEI showed during the historical episodes reviewed above. The index stretches back only to 1998, because the 45 indicators it tracks must be continuous and available in modern form throughout the entire period. Finding data series that meet both criteria before 1998 is not possible without compromising the index’s consistency. What the pre-1998 episodes do have, however, is the same underlying logic: the nominal economy was either strong enough to absorb the shock or it wasn’t, and the contemporaneous record reviewed here shows clearly that in each case the underlying conditions were deteriorating independently of oil before the recession arrived. The newspaper research and the NBER indicator analysis are doing what the LDEI would do if it existed back then.

Some use the Citi Economic Surprise Index as a proxy for tracking daily economic momentum. It is a reasonable facsimile to the LDEI but measures something different: how data compares to economist expectations, not the absolute level of nominal economic growth. When economists are pessimistic, even mediocre data produces a positive surprise reading. The LDEI measures growth directly and daily, making it a more natural, unbiased, and timely gauge of actual economic strength or weakness. When it falls substantially, that is the signal. Until then, it isn’t.

Right now, the LDEI shows an economy that is strong. The cycle within the cycle suggests growth continues until rates rise enough to stop it. A recession looks like an end of 2026 story, not a now story.

Oil gets the billing. The cycle is the real actor. And the variable that actually tells you when the story changes is the one almost nobody is watching.