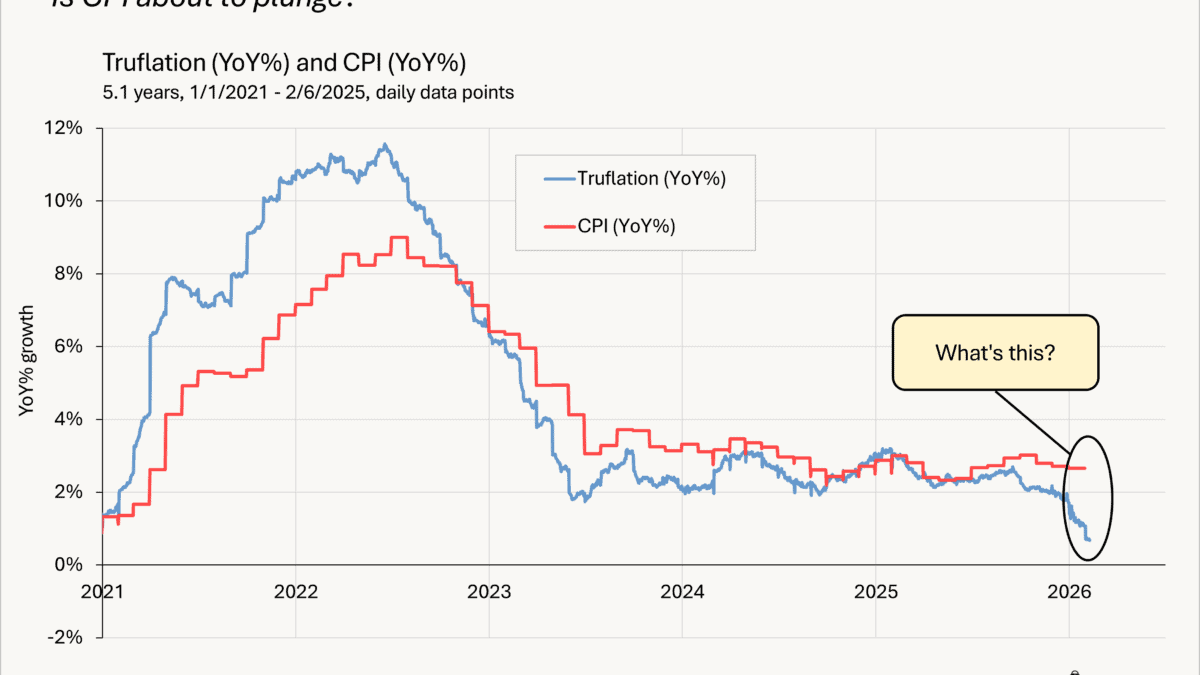

Skeptical of Truflation’s disinflation

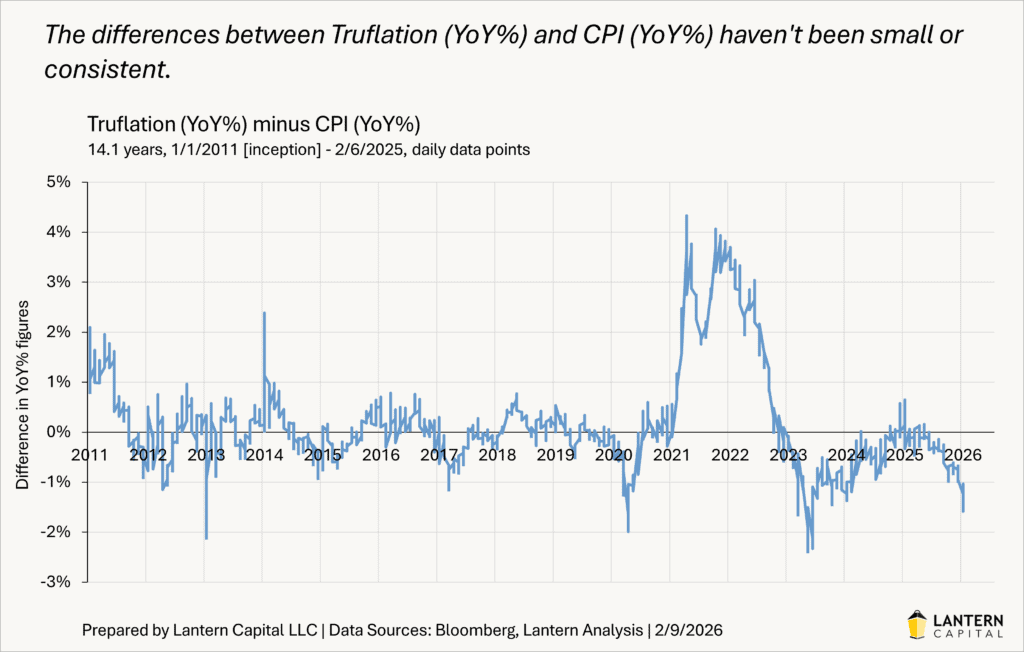

Truflation is a newer private real-time statistic of inflation that comes out each day (similar to the LDEI) with more granularity to see trends changing faster, be more timely, and fill-in when official data is absent (like last year’s government shutdown). Since its inception in 2010, the Truflation index (YoY%) has a correlation coefficient to the YoY headline CPI index of +0.92. While +0.92 is close to perfect, this figure still allows for large deviations from the CPI. The chart below shows the subtraction of Truflation (YoY%) minus CPI (YoY%), showing that the 0.92 correlation coefficient isn’t as locked together as one might expect. It is important to note that whenever Jerome Powell was asked about private-sector alternative data during the recent government shutdown, he never mentioned Truflation, in fact he never mentioned any name of a good inflation substitute. Truflation is materially different than the CPI because CPI uses surveys, observed prices, and imputations where things are missing, Truflation is purely observed prices from only digital transactions; credit cards, online prices, and private data feeds. CPI is a broader picture of inflation.

In recent months, Truflation’s YoY% has fallen dramatically from about 2.7% in September to 0.7% now. Everyone is wondering, “will CPI follow that?” According to the Cleveland Fed’s inflation nowcasts through February, they see headline CPI down to 2.3% from 2.7% and core CPI down to 2.5% from 2.6%, so they are seeing some disinflation, but nothing of the magnitude that Truflation is showing, and not much in the important and steadier core figure.

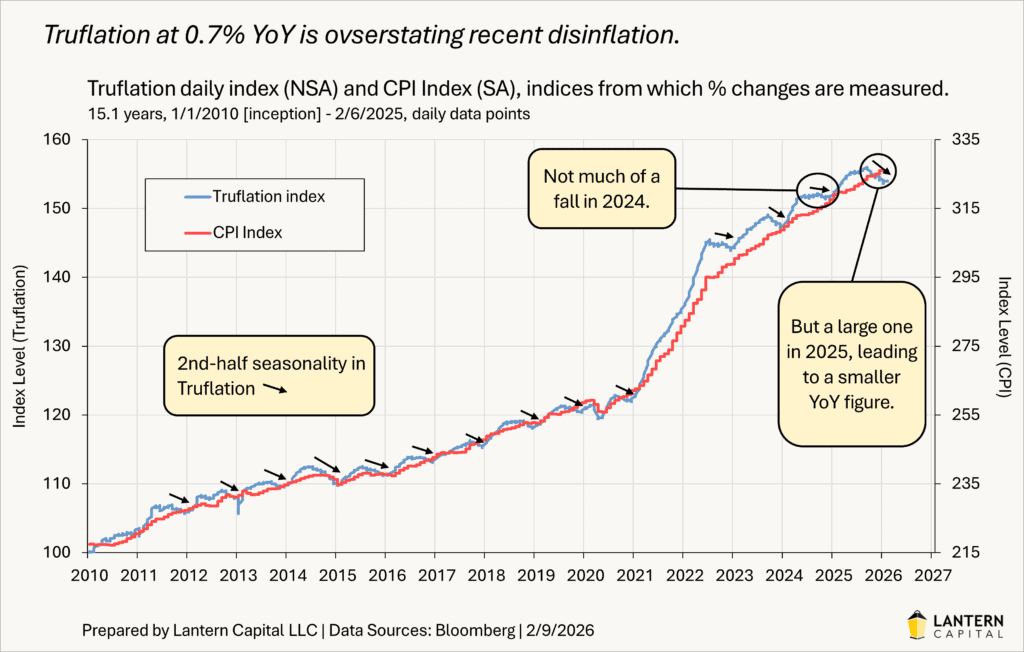

Unlike the CPI, Truflation isn’t seasonally adjusted. Theoretically, measuring a year-over year figure should nullify consistent seasonal effects, but they’ve been inconsistent over the last two years. The Truflation index has a consistent pattern of falling in the second half of the year from seasonality. You can see this in the black arrows in the chart below. Those second-half drawdowns vary somewhat over time, but average -0.8%. In 2024, there wasn’t much of a seasonal effect (-0.2%) versus a large one in 2025 (-1.0%). This discrepancy is creating a high base effect for Truflation’s YoY figure and lowering it. There is no way to precisely pinpoint the amount of the effect given all the moving parts, but Truflation is overstating disinflation.

Taking together the prior large deviations between Truflation and CPI, Powell’s non-endorsement, the Cleveland Fed nowcast numbers, Truflation’s seasonal base effect, and an expected boost to first-half economic activity, I don’t think YoY CPI inflation (headline or core) is headed below 2% in the near future. Truflation is a useful tool, but I am skeptical of how low its inflation figure is now for predicting what the CPI will become.