FOMC review: a hawkish committee with a new chair in tow

Warsh in the role

Back in January, former Atlanta Fed President, Raphael Bostic, made a great prediction about Kevin Warsh; to not take his job-auditioning comments too seriously. In an interview with CNBC on 1/30/2026, Bostic said,

I do think though, that we have to wait and see how people respond. The Federal Reserve is designed to have a different time horizon for its policy thinking than other policy makers. That creates tension, that is going to lead, inherently, to people having different views about what is important and how things should be weighted. We just have to see how Mr. Warsh is in the role. It is very interesting. When I was becoming, getting ready to become Atlanta Fed President, I had one set of thoughts and then when I became the president, you get to see things in a different way. So, I expect that to be exactly the same, and maybe even magnified as the chair of the Federal Reserve, and we’ll just have to see how things play out.

I wasn’t sure how far Warsh would go to please who appointed him, but Bostic was right, Warsh sounded like a serious Fed Chair today and mirrored the hawkishness of the committee. All of the themes he used to get the job: using a new inflation measure that’s conveniently lower, AI productivity being disinflationary to lower rates, and cutting rates while tightening the balance sheet were pushed into the future by his creation of five task forces to study the various bones he’s had to pick with the Fed (hopefully “concluding by year-end,” he said). They are:

1. Fed communications, does the Fed need to be transparent and give forward guidance?

2. Balance sheet, does it need to be this big?

3. Economic data, are there alternative data sources that are better than what is currently used?

4. Productivity, is AI going to be disinflationary? Will it reduce jobs?

5. Inflation framework, are there better measures of inflation? (like trimmed mean)

He can look, but I doubt Warsh is going to find much to change.

Hawkish Warsh

The press conference, summarized, was a response to Steve Liesman of CNBC,

And so, what you heard from the Committee today is, we’ve got some work to do on the price-stability front.

He repeated this commitment to price stability 11 times through the event, and there was a pointed sentence in the statement about it, “The Committee will deliver price stability”. He didn’t want to spell it out any more than this, but Warsh was hawkish in his first press conference.

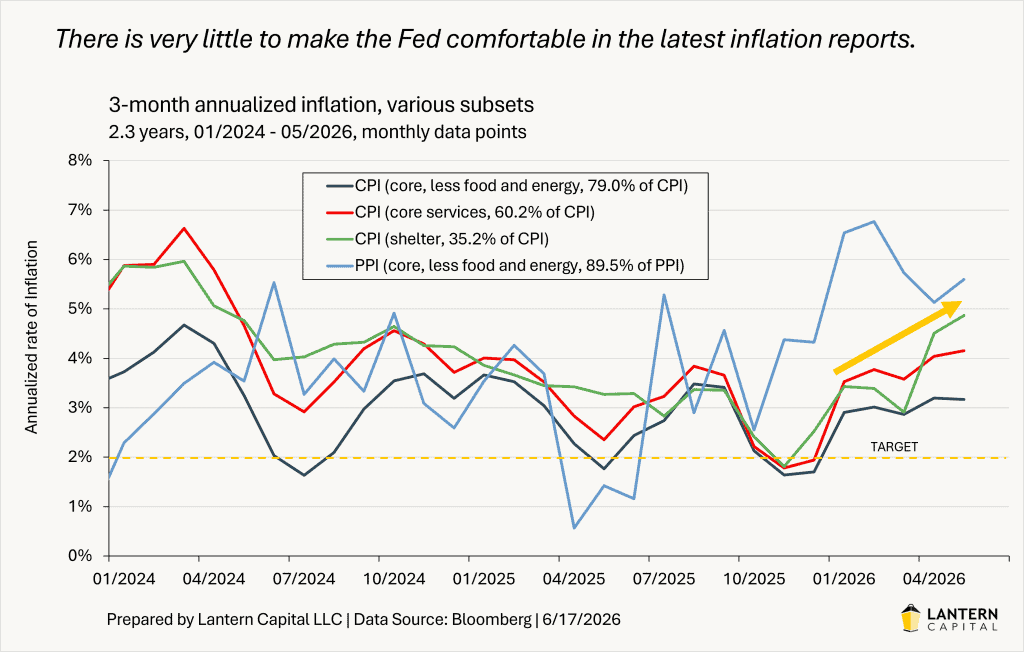

The committee was more forceful about it in the summary of economic projections (SEP). In them, the weighted average expectation for Fed Funds at the end of 2026 rose by a striking 48 basis points from the last SEP and rose 41 basis points for the end of 2027. Half of the Fed now expect rate hikes this year and a third expect two or more! For 2026 year-end Fed Funds, the market had only risen 34bps since the last SEP (3/18/2026) and cleanly, the 1-year and 2-year rose about 15 basis points today to fill that gap.

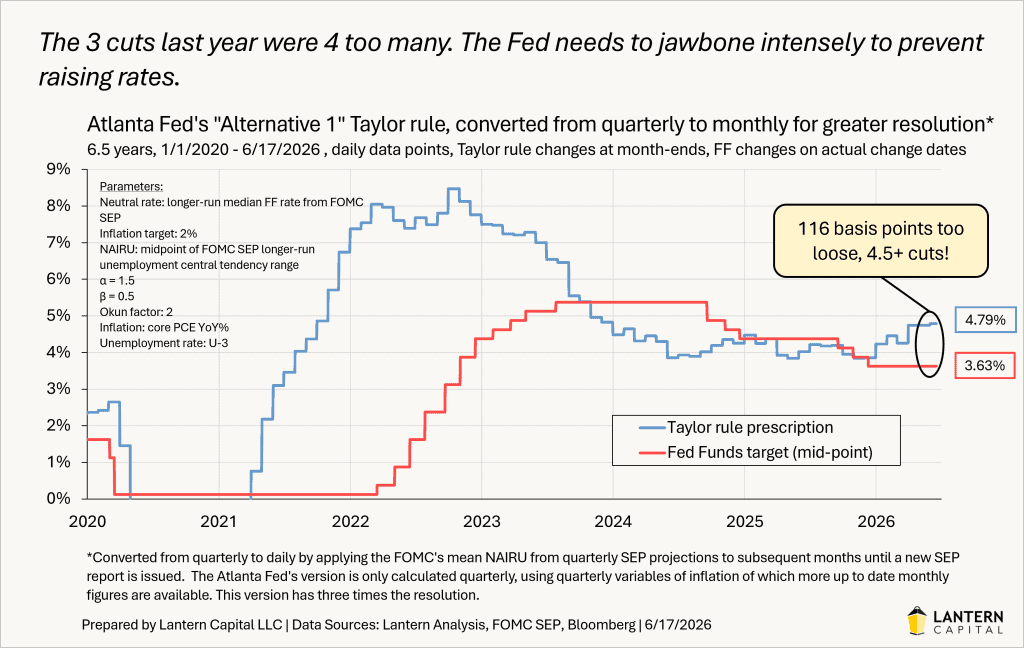

It was refreshing to hear, and it’s for a good reason. The Fed lowered rates too much last year and now there is inflation. Even the Administration has begun to pivot their messaging from lowering rates to bringing down inflation. Vice President JD Vance led with inflation concerns at his appearance on “The View” yesterday and after Warsh’s press conference, President Trump said “it could happen” that the Fed would have to raise rates. The Administration is very capable of switching from encouraging rate cuts to encouraging rate hikes for its best chance at the midterm elections.

What’s next?

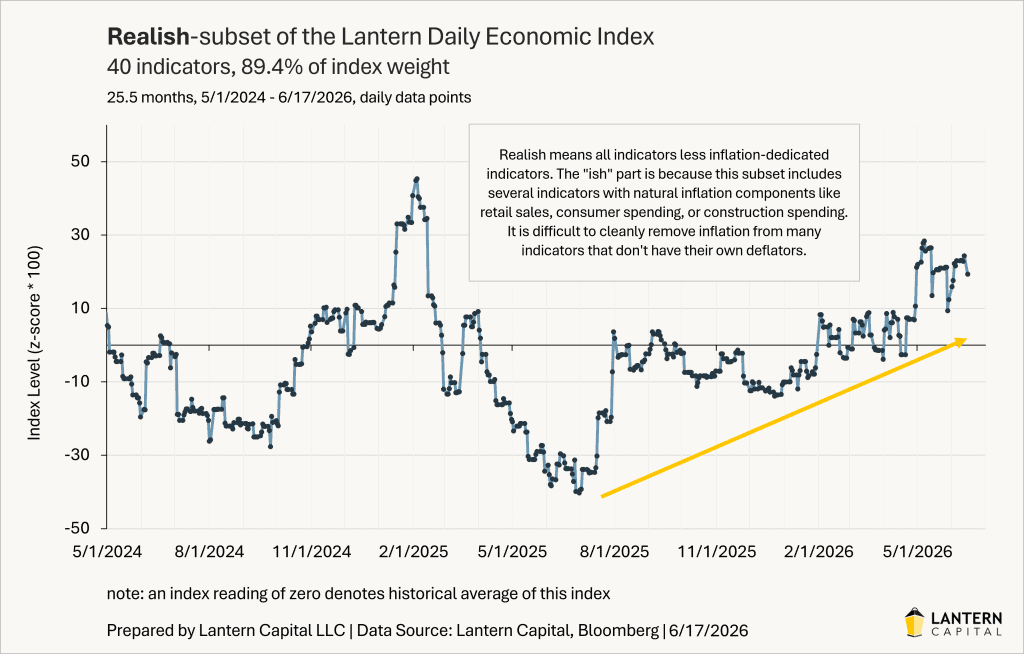

I continue to expect short-term rates to keep rising from here. My target on the 2-year is 4.40%. I doubt the Fed will actually raise rates, but they need markets to think they will, to slow down the economy again. I’ve expected a hot economy since last year from the ongoing “cycle within a cycle” from the high deficit and here it is. The data will likely remain hot until rates rise enough to slow the economy down again. Watch the LDEI for when that happens. The real economy hasn’t shown any signs of weakness yet.

This secondary trend of higher rates likely won’t be over until the consensus thinks rates need to be raised a lot; extrapolation. The narrative hasn’t gotten near that point yet, another reason why I think higher yields are still ahead.